Evolution (EVO/EVVTY) - Part 2

Evolution (EVO/EVVTY) - Part 2

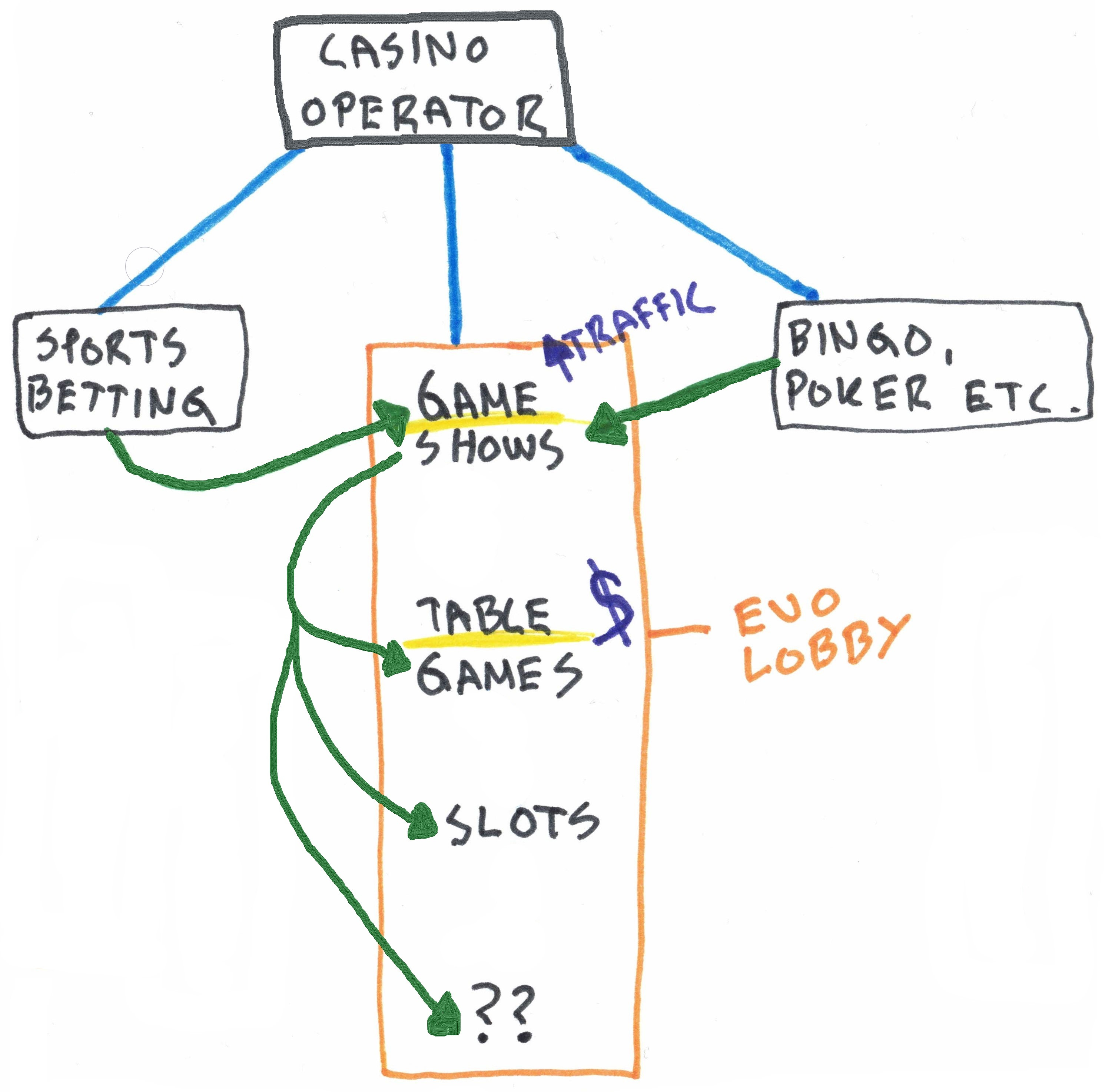

The Distribution Advantage

One of the key success factors for EVO has been market expansion by attracting a new type of player into the Live casino vertical partly via Game Show type games. In effect, EVO serves as a conversion tool of players from Sports betting, Slots, Bingo, etc., into Live Casino, a vertical which traditionally didn't lend itself to flashy marketing campaigns. Over the last few years, customer wins also confirm this, often citing Game Show innovation and its allure with players as key arguments.

In part 1, I wrote:

There are usually 3 games generating the bulk of the revenues in any Live Casino operation: Roulette, Blackjack, and Baccarat. Europe is all about Roulette, the USA is all about Blackjack, and Asia is all about Baccarat. These are the moneymaking games, while Live Game Shows are mostly conversion tools, first for converting sports players and subsequent cross-selling to table games with higher margins. In a competitive landscape like Online Casino, a differentiated offer for Blackjack and Roulette is hard, and regulation (where it applies) prohibits excessive promotions to players (Responsible Gaming). It is far easier to make a differentiated offer for Live Game Shows, and that's part of the reason why every provider needs to have this lineup of games, and why "lobby density" becomes increasingly important.

Game Show type games are a relatively new gaming category combining elements of both Roulette and Slots, bundling in an immersive AR experience, and plenty of in-game bonus elements adding additional novelty. The games are presented by a live host, and some are based on TV shows like Deal or No Deal. These games serve as effective conversion tools because they tend to broaden the funnel inviting new types of players and appealing to old players immersed in Roulette and Slots. Compared to Slots which is one-to-one experience, Game Shows is a one-to-many that allows for infinite scaling at zero marginal cost (assuming licensing costs are fixed).

In effect, they manage to replicate parts of the social experience of Las Vegas without the friction (traveling, hotels, etc.), combined with live streaming via Twitch/YT, straight from your living room with a couple of friends and a beer or two, like these guys having a good time..

As well as the natural tailwinds of land-based converting to online, I think the growth trajectory within online is where EVO will broaden the scope of the offering and expand into new verticals, e.g., news of NetEnt partnering with movie studios to develop movie-themed games or this recent job listing. Do I think the Vegas-type experience of going to a casino with your friends bundled with free drinks, hotel, and concerts are going away? Nope, but I do think Online casino is unlocking a new type of social experience without the friction where consumers will gradually adapt to new defaults. And once you reduce friction, it tends to unlock a non-linear change in behavior (and market size).

The Lobby Inside the Lobby

As a market leader in Live Casino, EVO leverages its scale in various ways. Keep in mind, for some of the smaller operators, the table revenue from EVO is north of 50%, including Slots (NetEnt/Red Tiger). A higher share of traffic, both direct, as discussed in part 1, but also via an increasing number of private tables, all begets more players. And once players are in an EVO game, they often stay in that ecosystem.

E.g., a sports player converted into an EVO game who chooses to exit (upper left corner) or go back to the lobby (down to the right) is not redirected back to the lobby of the operator but back to the lobby of EVO. In this way, games from either Playtech or Pragmatic are automatically "hidden behind the counter." Some of these redirecting shortcuts are unique to EVO, probably contractually, but some are also shared by Playtech and Pragmatic. This is also where lobby density comes into full play; a broader offering from internal IP development and acquisitions could easily be added to EVO's distribution rails (if licensed and agreed on), all contributing to a destination that ultimately covers all needs.

So, in essence, EVO is not only piggybacking the biggest cost items for the operator, customer acquisition, but they also serve as a necessary conversion tool, which adds traffic at the top of the funnel (game shows) and further cross-selling opportunities within the EVO ecosystem, inside the gates of the operator.

This brings me to my next point: EVO's bigger ambitions of becoming the world-leading provider of online casino games.

The BTG transaction announced in April adds one of the most innovative Slots players in the industry, growing 30-40% with EBIDTA margins around 88% with a team of 4 people. Total consideration up to EUR 450m with EUR 220m upfront (~35% cash and 65% shares), and the rest as earn-out (with 70% cash), at a price tag of 5-6x EBIDTA excluding earn-outs. So, on the surface, a seemingly easy add-on with low tech risk with a big portion of the purchase price tilted toward earn-out, which hedges risk for EVO. As CEO Martin Carlesund, mentioned under the Q1-21 call:

Of course, we see a potential to take BTG into our network, which is bigger than the current distribution channels that BTG have alone.

It's tempting to assume more bite-sized acquisitions in the pipeline allowing for favorable deal structures and multiple arbitrage, with low-risk integration to existing rails, where the sellers recognize the trajectory of the industry and hence want to come along for the ride.

The IMS Angle

The core offering for Playtech has been their own platform, i.e., their information management system (IMS). So, where EVO had a singular focus on Live casino, Playtech has always been a full-service provider with a broad range including Live, Slots, Bingo, etc. Think of IMS as a centralized platform with one view of the customer across games, which also handles cross-selling, various engagement tools, and bonus management, all limited to Playtech's own games. Playtech bundles their products and charges a certain percentage fee for the whole package, without distinguishing between the IMS platform and the games with a little extra charge for the fixed costs involved with Live casino. Playtech is famously known for their long contracts, sometimes 10-20 years, with one of their government monopolies across Europe.

In the future, EVO might be able to replicate some of the bonus management and promotional activities that Playtech offers within Slots through a product Red Tiger offers called Spark Insight. Perhaps EVO could leverage these tools across all verticals, with the goal of ultimately becoming the one-stop shop for their clients, further increasing the gap with competitors.

Disclaimer: Please do your own work, nothing here is investment advice. The author has a position in the stock.